How Much Do You Need Saved to Buy a Condo in Chicago?

by Daniel Ledo

How Much Do You Need Saved to Buy a Condo in Chicago?

If you're thinking about buying a condo in Chicago, one of the first questions is simple:

How much cash do I actually need saved?

The short answer: more than just your down payment.

Here’s a realistic breakdown of what buyers should expect in 2026.

1. Down Payment

Your down payment depends on the loan type and financial profile.

Typical Ranges:

-

3–5% down → Conventional first-time buyer programs

-

10% down → Common for Chicago condos

-

20% down → Avoids private mortgage insurance (PMI)

Example:

If you're buying a $350,000 condo:

-

5% down = $17,500

-

10% down = $35,000

-

20% down = $70,000

Many Chicago condo buildings require minimum down payments due to financing rules, so this must be verified early.

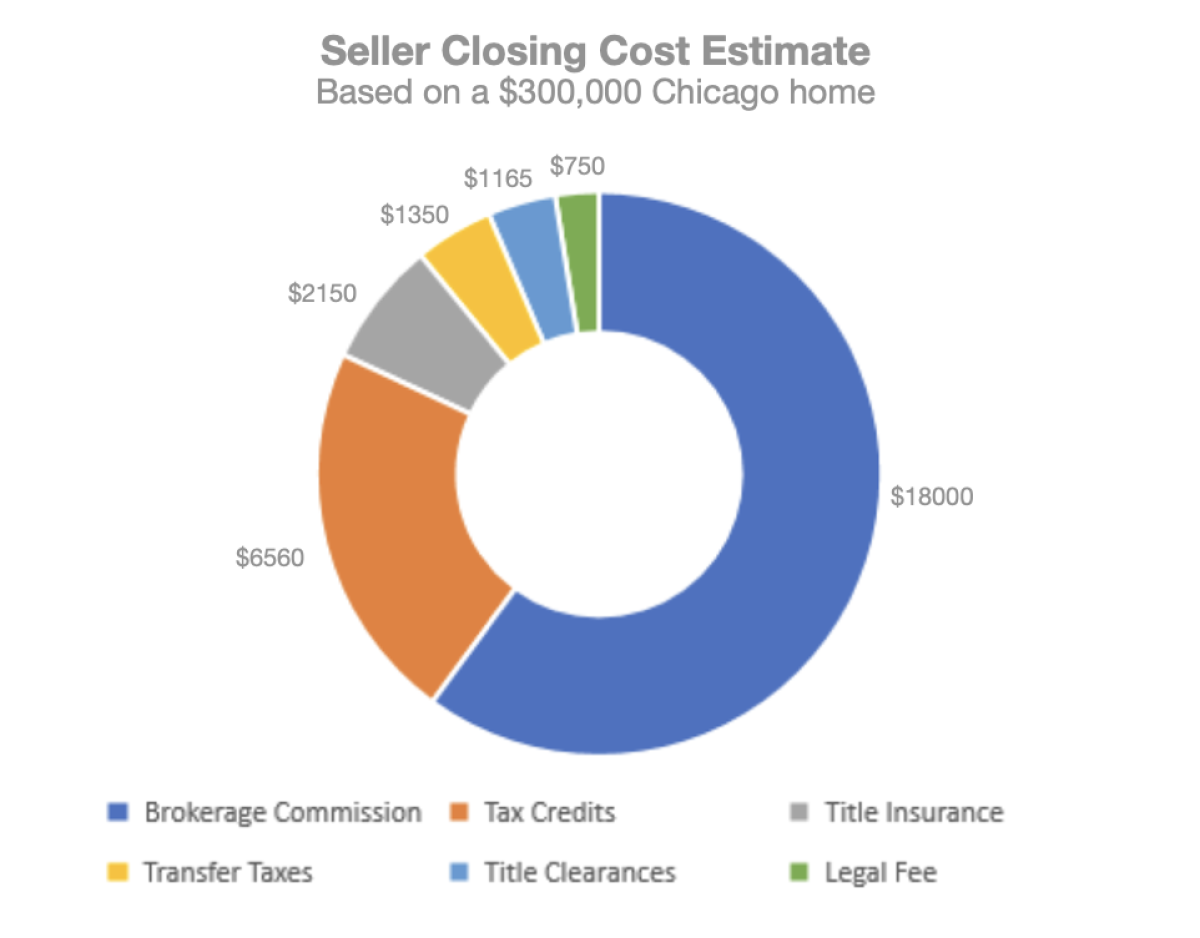

2. Closing Costs (2–4%)

Closing costs in Chicago typically run 2–4% of the purchase price.

On a $350,000 condo, expect:

-

$7,000–$14,000

This includes:

-

Lender fees

-

Title insurance

-

Attorney fees

-

Prepaid taxes

-

Escrows

3. HOA Move-In Fees & Building Costs

Chicago condos often include:

-

Move-in fees

-

Elevator deposits

-

HOA transfer fees

-

Paid assessment credits

These can range from $500 to $2,500+ depending on the building.

This is where many first-time buyers get surprised.

4. Post-Close Cushion (Highly Recommended)

Smart buyers keep:

-

2–6 months of expenses in reserves

Especially important for condos where:

-

Special assessments can occur

-

HOA dues may increase

-

Property taxes adjust

Financial stability = stress-free ownership.

5. Total Cash Needed Example

Let’s break down a realistic scenario:

$350,000 Chicago Condo

-

10% Down: $35,000

-

Closing Costs (~3%): $10,500

-

HOA/Move Fees: $1,500

-

Initial Reserve Cushion: $10,000

Total Suggested Savings: ~$57,000

That number varies—but this is a responsible benchmark.

What Impacts How Much You Need?

Several Chicago-specific factors matter:

-

Building owner-occupancy ratio

-

Rental restrictions

-

HOA reserves

-

Lender guidelines

-

Property tax proration

Condo purchases are more detailed than single-family homes because you’re buying into a building’s financial health.

The Bottom Line

To buy a condo in Chicago in 2026, most buyers should plan on having:

10–15% of the purchase price saved (minimum)

Closer to 15–20% for comfort and flexibility

The good news? Chicago still offers accessible entry points compared to many major cities.

Preparation is leverage. The more financially positioned you are, the stronger your negotiating power.

If you’re thinking about buying a condo in Chicago, the next step isn’t guessing—it’s running numbers specific to your budget and target buildings.

Want a custom estimate based on your price range?

Let’s map it out.

Recent Posts